》Check SMM silicon product quotes

》Subscribe to view historical price trends of SMM metal spot cargo

SMM News on June 19:

Since June, amidst the sharp decline in new order prices for PV glass, the number of enterprises conducting cold repairs and blockages of their kilns has begun to increase, marking the resumption of industry self-rescue efforts. According to SMM statistics, from June to date, nearly 20 domestic production lines have commenced blockages, and one kiln has undergone cold repair. Additionally, two more glass enterprises plan to implement blockages and reduce production in the future, involving a capacity of nearly 7,000 mt/day, leading to a reduction in supply.

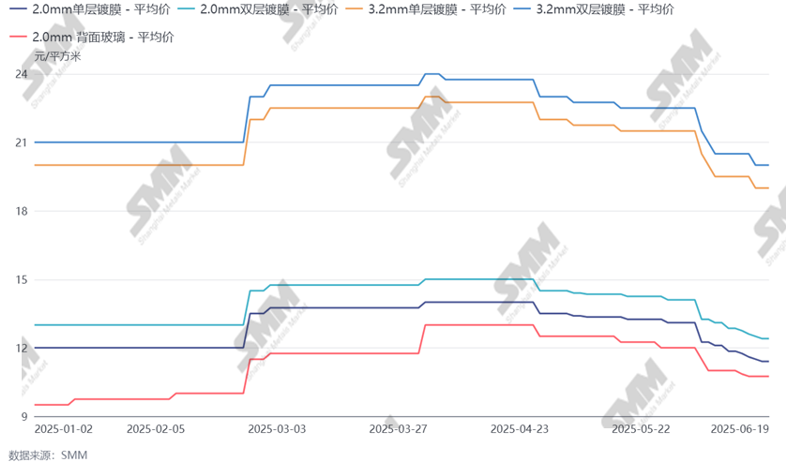

Figure: PV Glass Price Trend

Data Source: SMM

Since June, glass prices have been adjusted downward multiple times. At the beginning of the month, the quoted price for 2.0mm single-layer coated PV glass was 11.5-12 yuan/m². As of now, the benchmark transaction price for 2.0mm single-layer coated PV glass has dropped to 11.2 yuan/m². After enterprise agreements, there is still room for transaction discounts. According to SMM calculations, the current market transaction pricehas fallen below the enterprise cost line, causing most glass enterprises to shift from profit to loss. In terms of profits, with no discounts on raw materials such as electricity and quartz sand, enterprises have incurred losses of nearly 1 yuan/m² this month.

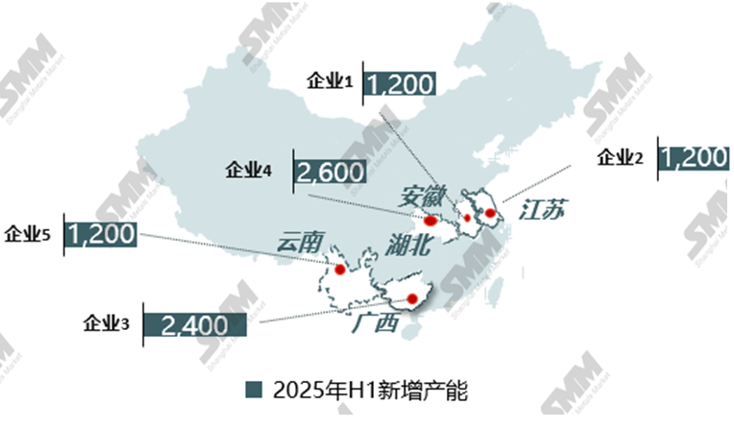

Figure: New PV Glass Capacity by Province in H1 2025

The main reason for the sudden reversal in the expected upward trend of glass prices is the excessively rapid release of new capacity! In the first half of this year, amidst the rapid upward trend in glass prices, some kilns that were previously constructed but had not yet started production began to start production. Additionally, kilns that had previously been blocked also resumed production, leading to a rapid increase in supply and leaving hidden dangers amidst the rising market trend. After experiencing policy-driven demand surges from the "430" and "531" policies, module demand quickly cooled down, while glass was in the phase of capacity release. The domestic supply-demand balance rapidly shifted to oversupply, causing prices to fall.

Figure: Cold Repair Capacity of PV Glass by Province in H1 2025

In contrast, some glass enterprises had already identified hidden dangers in the H1 stage and began to conduct cold repairs and production cuts. However, the overall production cuts were still relatively small. With the continuous decline in prices this month, the intensity of glass production cuts has increased again. However, for the supply-demand balance forecast in Q3, the module production cut speed remains relatively fast, and the self-rescue production cuts by glass enterprisescan only halt the price decline but cannot "reverse the trend", with actual supply still showing a surplus. Therefore, we can only wait for subsequent changes in the supply side.

Regarding future supply, although the intensity of this round of production cuts is not weak, the actual monthly supply will still be around 46GW, leaving some room compared to demand. After the next round of production cuts takes effect, it is expected that the glass market will slightly improve in Q3, but it will only oscillate near the cost line. The actual reversal signal still depends on the module improvement amplitude driven by the installation rush in Q4. In conclusion, "Enduring countless hardships, I remain resilient, defying winds from all directions—east, south, west, and north." Glass still holds the hope of blossoming anew in the cold winter season.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)